Ship Backup at Southern California Ports Is Receding

Cargo has increasingly generated significant revenue for Indian airlines, especially after the global pandemic. As the world embraces globalization, India’s air cargo sector is rapidly growing, establishing itself as a leading industry player.

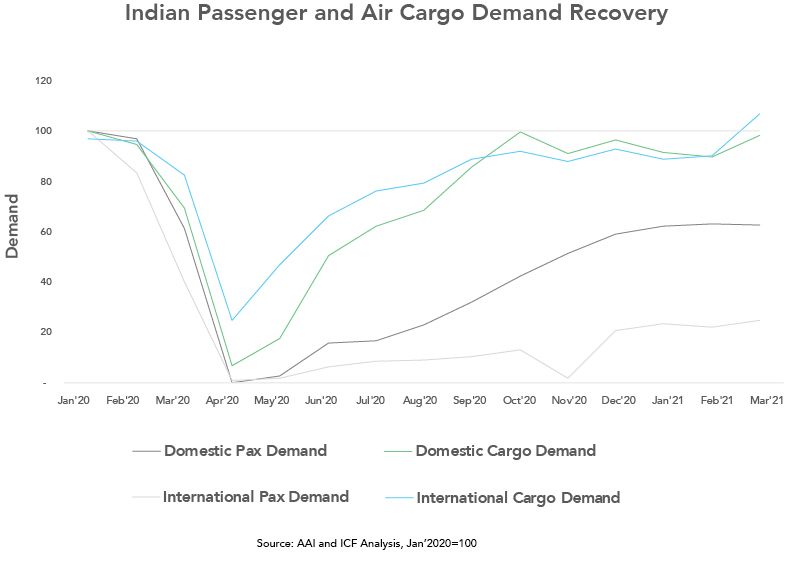

Pre-COVID: Passenger-Driven, Cargo Neglected

Before the COVID-19 pandemic, the Indian aviation industry focused primarily on passengers, achieving remarkable growth. Indian passenger airlines saw a 12% Compound Annual Growth Rate (CAGR) between 2009 and 2019. Despite this focus, the industry neglected the cargo market, although it still grew at a respectable 8% CAGR over the same period.

Passenger volumes plummeted by nearly 70% in 2020 due to the pandemic, forcing airlines to rethink their business models. As passenger airlines struggled to stay viable, air cargo gained importance and moved into the spotlight. Prior to the pandemic, Indian air cargo faced significant competition from ocean freight and rail transport, with only one dedicated cargo airline, Blue Dart, operating since 1996.

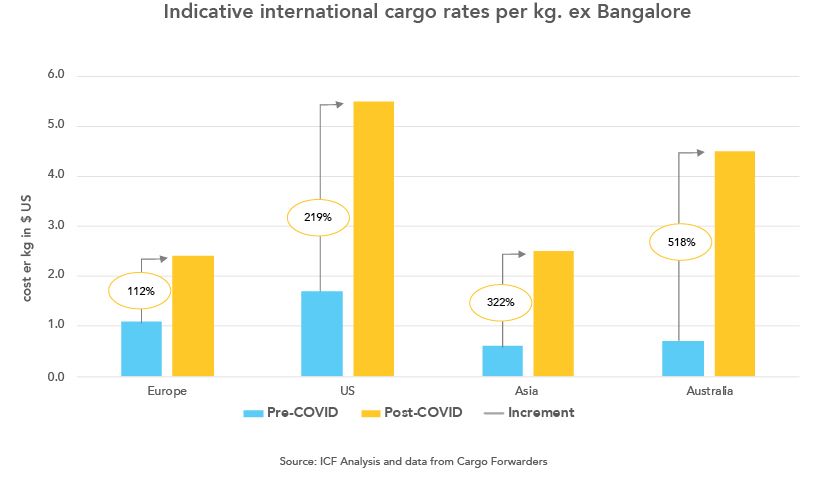

Air Cargo’s Growth During the Pandemic

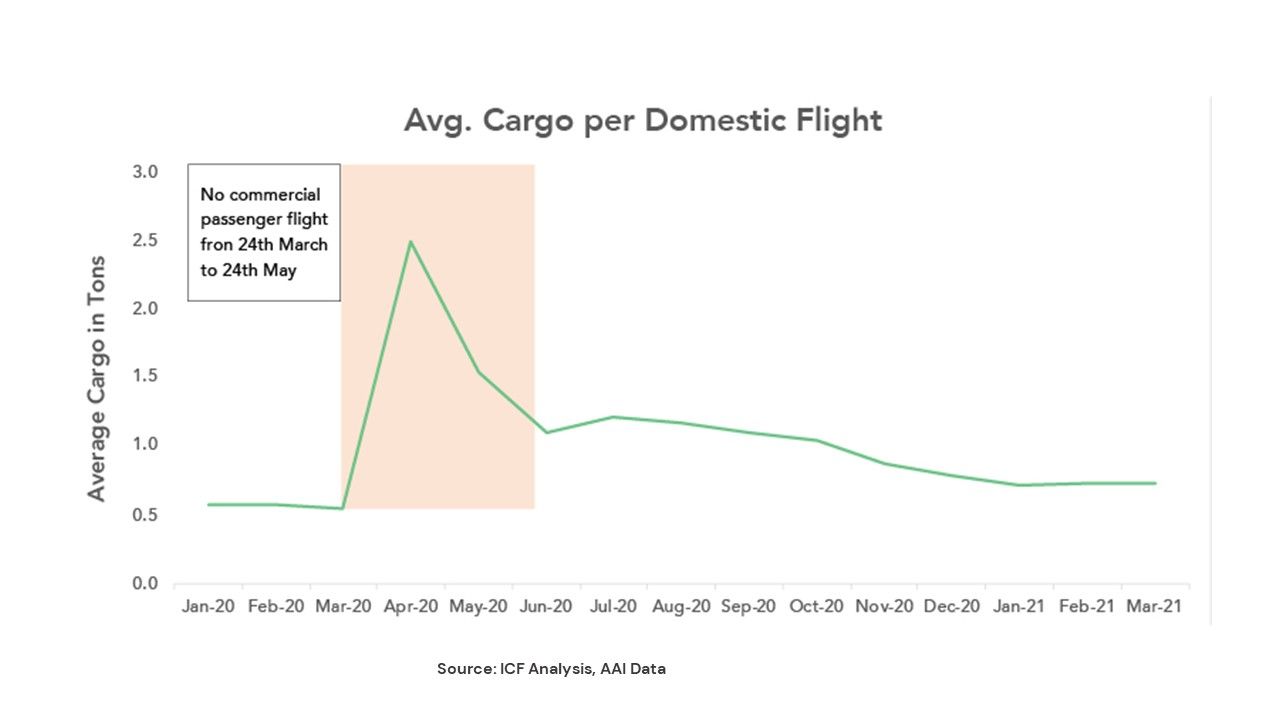

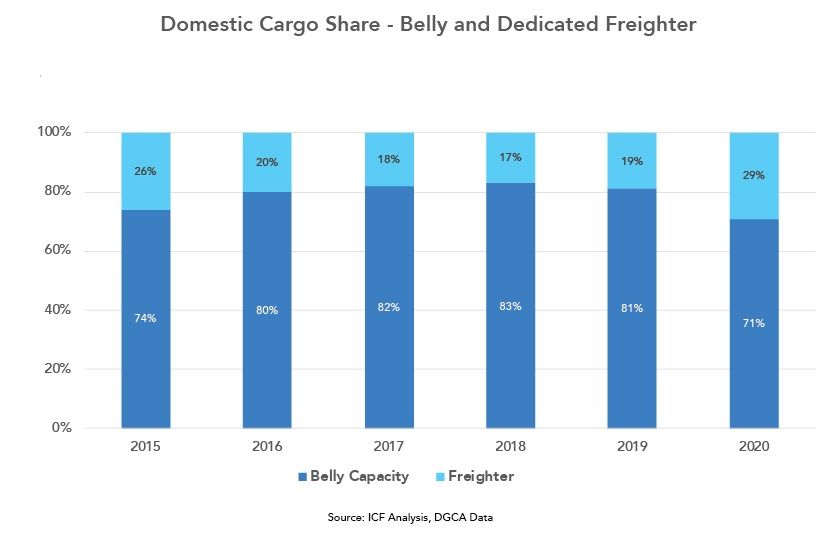

The reliance on bellyhold cargo in passenger aircraft was a major factor limiting air cargo growth. The pandemic, however, triggered a sea change. Passenger airlines, like SpiceJet, quickly pivoted by launching their own dedicated cargo subsidiary, SpiceXpress, and expanding their fleet with B737s, Q400s, and widebody aircraft like B767s and A330s. This diversification allowed them to offer door-to-door services, increasing their cargo market share.

Infrastructure Development and Air Cargo’s New Role

In response to the growing demand for air cargo, India has rapidly enhanced its airport cargo infrastructure, expanded digital solutions for cargo handling, and fostered collaborative partnerships between stakeholders. Despite these advancements, challenges remain, particularly as the cargo sector works to keep pace with the rising demand from industries like e-commerce and pharmaceuticals.

Demand Drivers: E-Commerce and Pharmaceuticals

The pandemic fundamentally altered consumer behaviour, accelerating the shift toward online shopping. Increased digital literacy in both urban and rural India has fueled the growth of e-commerce, which is expected to grow fivefold by 2026, reaching a market size of $200 billion.

The pharmaceutical industry in India also plays a key role in the air cargo boom. Known as the “Pharmacy to the World,” India is the largest global provider of generic drugs, contributing 50% of the world’s total demand. Export volumes increased by 18% in the last financial year, and the domestic pharmaceutical market is set to triple by 2030.

Both e-commerce and pharmaceuticals rely heavily on air cargo for quick and reliable transport, further bolstering the growth of air cargo in India.

Air Cargo: A Lifeline for Indian Airlines During the Pandemic

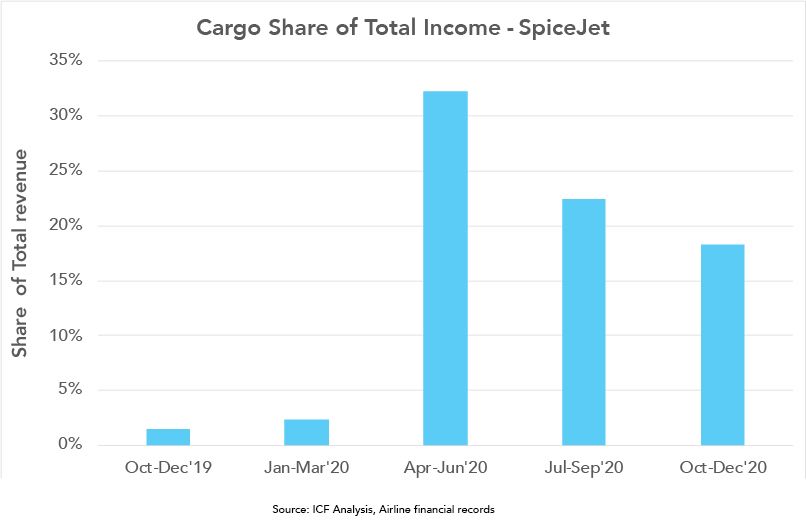

With passenger demand falling sharply, airlines shifted their focus to cargo operations to sustain their businesses. For example, SpiceJet reported a 450% increase in cargo revenue in the last quarter of 2020, and cargo operations contributed to 32% of the airline’s total revenue. Airlines like IndiGo also adapted by converting passenger aircraft to freighters, ensuring their survival during the pandemic.

Challenges and Opportunities in Air Cargo

The rapid rise in air cargo demand has forced Indian airports to expand their cargo-handling capabilities. Infrastructural investments, such as dedicated terminals for temperature-sensitive pharmaceuticals and express e-commerce cargo, have improved the speed and efficiency of cargo operations. However, challenges remain, such as disrupted flight schedules, high cargo prices, and limited freighter capacity, making it essential for the sector to adapt.

India, despite its geographical advantages, still lacks a dedicated freighter airline sector, which could significantly boost the country’s position as a global cargo hub.

Post-Pandemic Outlook: The Future of Air Cargo

The air cargo sector in India is poised for substantial growth post-pandemic. However, in order to maintain this growth, the sector will need to address challenges such as high fuel costs, increased competition, and the lack of dedicated freight capacity.

One key driver of future growth will be digitization, enabling end-to-end paperless operations and the seamless integration of the entire supply chain. This will lead to higher efficiency, reduced dwell times, and lower overall costs.

E-commerce, in particular, is set to drive demand for air cargo in the coming years, requiring airlines to expand their cargo capacity and form strategic partnerships with e-commerce giants like Flipkart and Amazon. International airports will also need to expand their infrastructure and create dedicated facilities for special cargo categories.

Conclusion

The Indian air cargo industry has enormous untapped potential. To capitalize on this, airlines must invest in dedicated freighter aircraft and infrastructure improvements, while also embracing digital transformation. By doing so, India can emerge as a key player in global air cargo logistics, meeting the growing demands of the e-commerce and pharmaceutical industries.

Air cargo’s rapid growth will play a crucial role in shaping the future of Indian aviation, but achieving sustainable growth will require significant sector reforms and infrastructural investments.

Related posts

Southern California Port Congestion Begins to Ease

The extended backlog of container ships waiting to unload at the Southern Califo

Why Partnering with a Trusted Cargo Partner in India Can Transform Your Supply Chain

In today’s rapidly evolving global market, India’s logistics industry is und

Ship Emission Compliances as per MARPOL 2020: Navigating the Waters of IMO 2020

The International Maritime Organization (IMO) introduced one of the most signifi